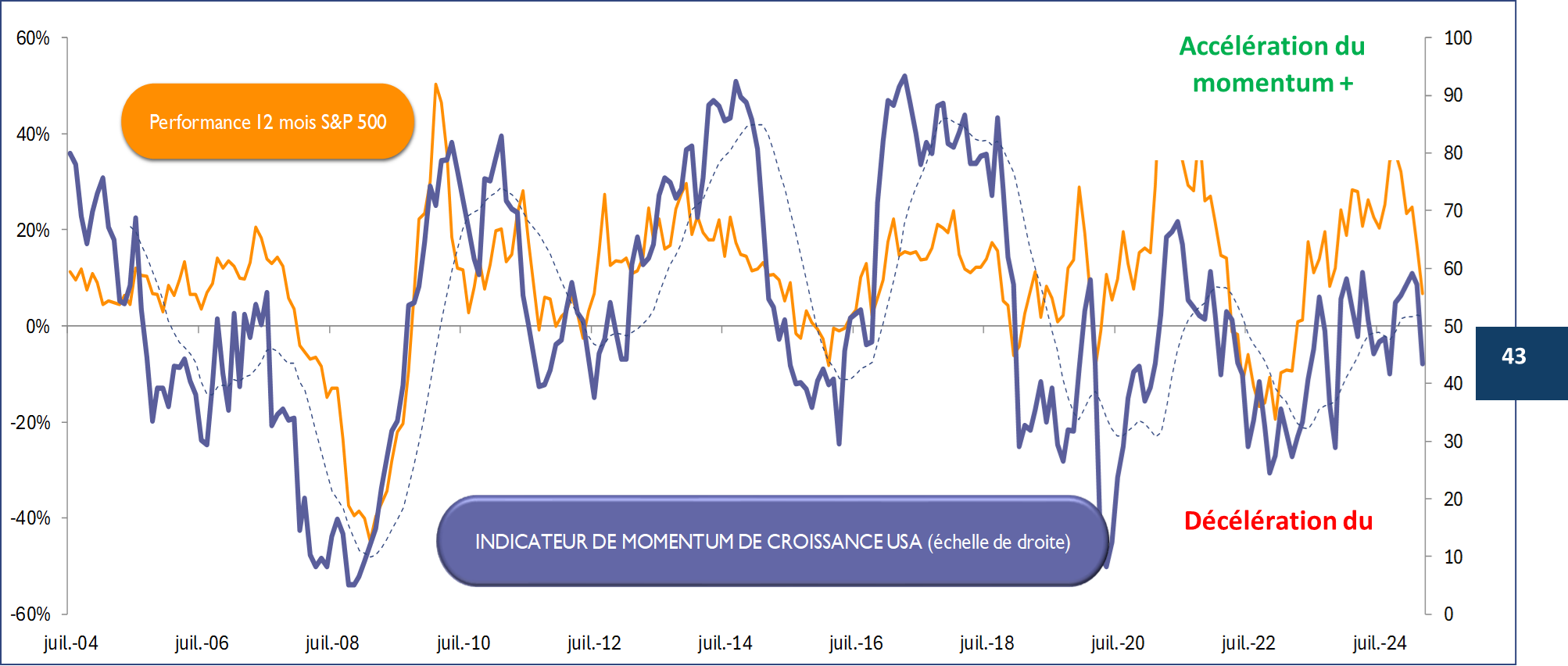

The American engine is running out of steam. For several weeks now, signs of a slowdown have been multiplying across the Atlantic. Long considered an unshakable safe haven for global investors seeking growth, the country is now beginning to doubt. Our Montpensier Arbevel Economic Momentum Indicator, at 43, is now clearly in contraction territory.

Source : Bloomberg / Montpensier Arbevel as of 28 march 2025

The American engine is running out of steam. For several weeks now, signs of a slowdown have been multiplying across the Atlantic. Long considered an unshakable haven for global investors in search of growth, the country is now beginning to doubt. Our Montpensier Arbevel Economic Momentum Indicator, at 43, is now clearly in contraction territory.

Surveys confirm this wait-and-see sentiment. The two most recent reports from the University of Michigan and the Conference Board both show that consumer confidence is falling sharply, and that their outlook is clouded by record levels of uncertainty.

Among businesses, the trend is similar, although absolute levels remained reassuring prior to the tariff announcements. Purchasing managers in the manufacturing sector, surveyed in March by S&P as part of the PMI reports, are less optimistic than their counterparts in services, who still help keep the composite indicator at 53.5 – clearly above the expansion threshold.

Although they also show a weakening of momentum, “hard” data, which measures the various components of national activity, are less conclusive. Weekly jobless claims remain low, housing activity is holding up, and retail sales are still resilient. The only notable concern is consumer spending in bars and restaurants, which dropped significantly in March — potentially an early signal of growing caution.

This trend confirms the gradual exhaustion of the extraordinary — and largely unsustainable — growth pace seen in the U.S. over the past two years. At 3.4% last year, growth was estimated to be about 1 percentage point above the country’s potential, given its production factors and productivity.

However, the unprecedented scale of tariff hikes announced by the Trump administration on April 2 — which could push tariffs to their highest levels in a century — along with the potential escalation of retaliatory measures, raises growing concerns.

The automotive sector is a striking example. If all taxes announced by the President between the U.S., Canada, and Mexico (excluding the April 2 measures) are considered, the average vehicle price would rise by $6,000, according to the American Automotive Association — and by as much as $9,000 for SUVs, which are particularly popular in North America. This would significantly dampen consumer buying intentions.

As a result, by the end of March, indices measuring uncertainty about economic and trade policy had already reached record levels — not seen since the pandemic, and in the case of trade policy, not since the 2008 crisis.

Yet consumers represent only the visible tip of the iceberg when it comes to the impact of tariffs. According to research and analysis firm Alpine Macro, only 4% of total U.S. consumption would be directly affected by the measures proposed by Donald Trump.

In contrast, the impact on businesses could be much greater. Alpine Macro estimates that 16% of business activity could be affected. This means the main economic impact would likely be felt through this channel: pressure on margins, investment, and hiring — all depending on how economic agents respond. The veil of uncertainty is thickening, as evidenced by a sharp correction in equity indices on Wall Street since the beginning of the year.

The key question now is: how resilient are the fundamentals of the U.S. economy in the face of this trade storm?

Several indicators will be worth monitoring:

1-Small business sentiment, as measured by the NFIB index. At 100.7 in February, it declined by 2.1 points in one month and hit its lowest level since the November elections — but still stands well above the 2022–2024 average of around 90.

2-Temporary employment trends in the labor market. After falling sharply from January 2022 and turning negative in the summer of 2024, it had been improving over the past three months — a signal, until now, of resilient economic activity.

The balance sheets of businesses and households remain solid, which should help prevent the trade crisis from morphing into a financial one. High-yield credit spreads remain contained, and household debt service ratios, at 11%, while rising over the past two years, are still below pre-pandemic levels.

Despite concerns triggered by “Liberation Day”, the situation is, for now, not yet alarming. However, two factors remain critical and must be closely watched:

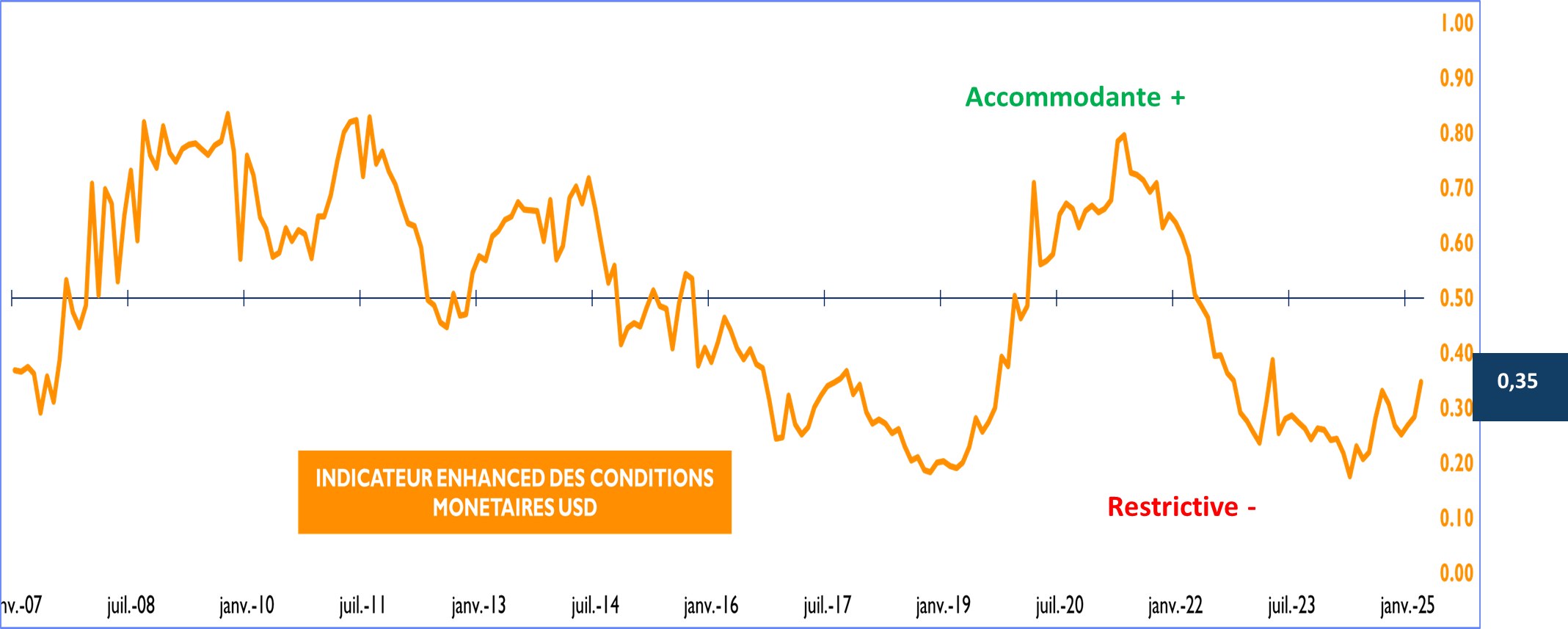

1-The evolution of financing conditions in the U.S. economy. So far, so good: although our Montpensier Arbevel Monetary Conditions Indicator remains in restrictive territory, falling interest rates and a weaker dollar are gradually creating room for more easing. The announced slowdown in the Fed’s balance sheet reduction program should also support this trend.

Source : Bloomberg / Montpensier Arbevel au 28 mars 2025

2-The second issue is the evolution of the Trump administration’s economic doctrine regarding the dollar and interest rates — and this is where concern is rising.

Until now, trade policy could still be seen as consistent with the 47th president’s usual negotiation tactics: taking maximalist positions to extract tangible concessions — much like the U.S. capital-backed control of the Panama Canal or the talks initiated with China over TikTok.

However, a deeper question is beginning to emerge: Could the real aim of the “sound and fury” around tariffs actually be to lower interest rates and weaken the dollar ?

Indeed, White House economic adviser Stephen Miran — when he was a strategist at hedge fund Hudson Bay Capital — never hid his view that the U.S. should engineer a new “Plaza Accord” to drive down the dollar and reduce debt servicing costs by “forcing” the conversion of existing Treasury bonds into perpetual zero-coupon bonds.

Such a move would profoundly destabilize America’s role as the world’s financial center. We’re not there yet — but the mere possibility is unsettling.

Markets are now eagerly awaiting a return to calm and clarity. The Federal Reserve could help restore some visibility — and perhaps even the European Central Bank, starting April 17?