Jevons’ Paradox Illustrated in the Cloud

Between 2016 and 2020, the average cost of a gigabyte of cloud storage dropped from approximately $0.15 to $0.02, while data center energy consumption surged from 120 TWh to 270 TWh. Despite improved efficiency and lower unit costs, the resulting democratization—making these services accessible to a larger audience—has driven demand higher, ultimately increasing overall energy consumption. (Sources: Leading cloud providers AWS, Azure, Google Cloud; International Energy Agency, 2021)

This pattern is likely to repeat with AI. Thanks to the sharp decline in inference costs, as demonstrated by DeepSeek, businesses will find it much easier to integrate generative AI into all their applications.

AI and Data Centers Driving Electricity and Energy Demand

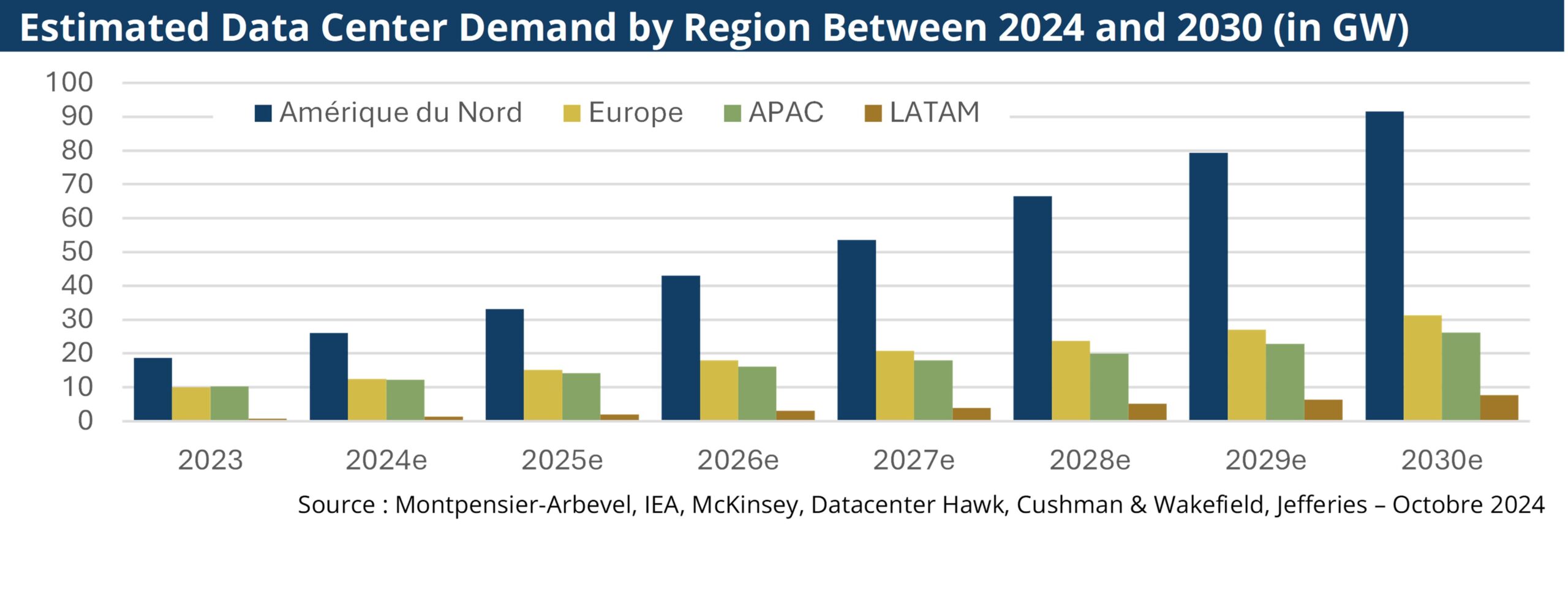

Data centers, a sector currently growing at 15% annually in terms of capacity, already consume 4% of the electricity produced in the United States—a figure expected to rise to 9% by 2030 (source: Electric Power Research Institute, EPRI). In October 2024, Microsoft, Google, and Amazon successively signed Power Purchase Agreements (PPAs) totaling 2.7 gigawatts, enough to power over two million homes. Amazon is already the world’s largest corporate buyer of solar and wind electricity, aligning with its 2040 carbon neutrality target (2030 for Google). Meanwhile, Microsoft aims to achieve a negative carbon footprint within the next five years.

Iberdrola, for its part, has already secured a pipeline of more than 5 GW dedicated to data centers in Spain, as European data center energy demand is expected to double by 2026.

On a global scale, despite advancements in hardware efficiency, the expected doubling of electricity consumption due to data centers and AI within five years would represent the energy demand of a country like Japan (about 150 GW, the world’s fifth-largest electricity consumer). This presents an unsolvable challenge in the context of the energy transition. It is virtually impossible to generate the required low-carbon electricity within just a few years.

Moreover, the need to simultaneously produce enough clean electricity to meet the growing “normal” demand—driven by new mobility solutions and technological applications—while replacing thermal power plants adds further pressure. The annual growth rate of electricity demand in the next six years is expected to be six times higher than in the past two decades in the United States (a trend that extends globally), as highlighted by Eaton, a U.S. specialist in electrical infrastructure, during its investor day this month.

Opportunities for Utilities, SMRs, and Data Centers

The growing need for large-scale electricity to support the development of data centers reinforces Jevons’ Paradox mentioned earlier. Ultimately, the emergence of DeepSeek and the broader expansion of artificial intelligence could signal a new cycle of visible growth for utilities. These companies, often overlooked in stock markets and significantly undervalued compared to some tech or industrial firms (trading at an average 15.6x forward 12-month PE versus 18.9x for the MSCI World), could regain long-term investor interest.

In response to the rising demand for stable and decarbonized energy, Small Modular Reactors (SMRs) are attracting increasing attention from hyperscalers (e.g., Google’s investment in Kairos Power). These small-scale nuclear reactors, designed for mass production and on-site assembly, offer a more flexible and potentially faster-to-deploy alternative to traditional nuclear power plants. Hyperscalers, which account for 70% of infrastructure spending (Synergy Research Group), are looking for ways to achieve energy autonomy without destabilizing electrical grids. However, SMR technology is still in its early stages, with few commercial deployments and uncertainties regarding cost models.

According to the Uptime Institute, a leading data center certification body, 50% of new data centers will generate a portion of their energy on-site starting this year. Additionally, the European REPowerEU directive mandates that 90% of new data centers must be carbon-neutral.

With the rise of generative AI and the planned investments to expand storage and computing capacity, growth prospects remain strong for companies operating in the data center market. In this context, Vertiv, a global leader in critical data center infrastructure, is particularly well-positioned to benefit from this trend. The company specializes in power supply solutions (34% of revenue) and cooling systems (30%) and offers innovative products that can reduce energy consumption by approximately 20% and optimize space usage by up to 70%. Notable solutions include Vertiv Liebert AFC (air/water compressor) and Vertiv PowerNexus (next-generation UPS).

Strong Business Outlook

Vertiv’s growth prospects remain solid. In its latest quarterly earnings report, management reported revenue growth of 23% to 32% across different regions, with strong cost management, leading to an operating margin of 21.5%. Additionally, deleveraging efforts have strengthened the company’s financial position, reducing leverage from 5.6x in 2022 to 1x in 2024.

Despite trading at an average 33x forward PE over the past year, the announcement of DeepSeek has devalued the stock to a forward PE multiple of 21x. This trend has also affected other data center-exposed stocks, such as Schneider Electric, which generates 20% of its revenue from this segment, with half coming from hyperscalers (Source: company data, end of 2024).

Attractive Investment Opportunities Across Multiple Themes

While DeepSeek may have unsettled investors, companies remain confident in the continued construction of data centers and rising energy demand. The recent derating of certain stocks could present attractive opportunities for thematic funds exposed to these secular growth trends, including: Pluvalca Global Trends (Data Center & Energy exposure: 15%), M Climate Solutions (Data Center & Energy exposure: 23%), M Cloud Leaders (Data Center & Energy exposure: 29%), M Global Onshoring (Data Center & Energy exposure: 21%), Pluvalca Global Blockchain Equity (Data Center exposure: 13%)*

*Source: Montpensier Arbevel, as of March 14, 2025.